Companies need to register for VAT (IVA) purposes with the local tax authorities in Spain and they have to take the necessary measures so that their business complies with the tax regulations in their business field.

Our team of specialists in company registration in Spain can advise on the tax registration procedures that are applicable for the VAT – IVA tax in Spain; investors can obtain consultancy services from our specialists that are related to all the corporate taxes that have to be paid by local businesses.

Table of Contents

VAT rates (IVA tax in Spain)

The Spanish value-added tax has a standard value of 21% for most goods and services, but reduced rates of 10% and 4% also apply. 10% reduced VAT applies for passenger transport, certain plants, amateur sporting, and events.

Basic foods in Spain are exempt from VAT taxation since 2023. This measure is valid until June 2024. However, health products and electricity will no longer benefit from reduced VAT.

Starting with January 2024, the VAT for electricity services is set at 10% instead of 5% for the previous year. As such, the Spanish Tax Agency will collect around EUR 1.016 billion from VAT on electricity in 2024, and about EUR 397 million from the VAT on gas, wood, and pellets for heating.

According to recent tax modifications, only certain clients like the ones on welfare support and low incomes, plus small businesses can benefit from an electricity price ceiling of around EUR 45 per MWh in the marketplace.

Bookkeeping in Spain is necessary for the good running of a company, from a financial point of view. Thus, all financial operations are registered in the company, and the respective documents will help in the preparation of annual financial statements and submission to the revealing authorities. Ask our certified accountants about the services we can offer for your company in Spain. You can also benefit from a free case evaluation in order to understand the financial needs of your business.

What should Spanish businesses do once they are registered for VAT?

Businessmen who want to open a company in Spain in 2024 should know that once their business was registered for VAT purposes, specific procedures must be completed. Our team of consultants in company formation in Spain can offer step-to-step advice on the following procedures, which must be completed by all VAT payers in this country:

- issue invoices specifying the disclosure details, as per the Spanish tax legislation;

- issue electronic invoices containing specific aspects, such as the electronic signature;

- keeping and maintaining the company’s accounts and records, for a period of 10 years;

- issue invoices for customers buying goods or services in Spain;

- process credit notes and using the correct foreign currency rates.

Since when is the VAT applicable in Spain?

The authorities have introduced the IVA tax in Spain in 1986 when the country became a member state of the European Union (EU); the current legislation on VAT includes the regulations prescribed at the level of the EU and it regulates the manner in which commercial entities have to register for VAT, comply with the local VAT rules and submit VAT returns. The main institution which is in charge of the VAT regulations and compliance is the Agencia Estatal de Administracion Tributaria. Once registered for VAT, the following will apply:

- a company must deposit quarterly VAT returns provided that it had in the previous financial year a turnover of a maximum of EUR 6 million;

- the monthly quarterly returns have to be completed by Spanish businesses which obtained a turnover of above EUR 6 million;

- provided that a company in Spain does not respect the reporting requirements, they can be charged with fines ranging from 20% to 200%, applicable to the VAT they should have reported;

- late payments of VAT can also be imposed with an interesting fine of 5% (for a delay of one month);

- the value of the interest fine can increase up to 20% in the case in which the company delayed the payment of the VAT for a year.

What types of entities should register for IVA tax in Spain?

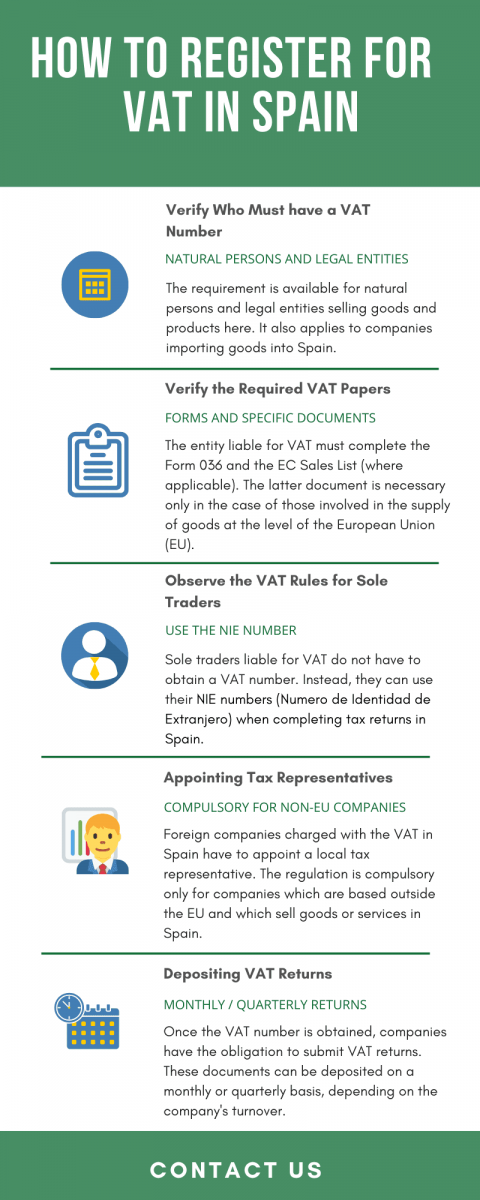

As a general rule, commercial entities obtaining taxable income from the sale of goods and services in Spain are required to register for VAT. Below, we present the main categories of commercial entities that have to apply for a VAT number in order to pay VAT in Spain:

- companies importing goods on the Spanish territory, even in the case in which the goods are to be sold on another EU market;

- entities selling goods or services (and entities purchasing goods and services) which are not Spanish companies that were issued with a VAT number;

- the sale of goods and services through the internet is also charged with the VAT;

- companies storing goods in warehouses in Spain, as these premises are considered permanent establishments;

- companies organizing live events and exhibitions which charge admission fees to such events.

Those entities that are liable for the payment of VAT should take the necessary measures in order to register for the payment of this tax. This is also necessary for foreign entities selling goods on the Spanish market. As a foreign trader, VAT registration in Spain in 2024 is done by completing Form 036, a document that must be signed and submitted. This can be done in person or by accessing the online platforms of Spanish tax institutions.

This document will also be used for assigning a Spanish VAT number and no other additional documents will be required. The VAT identification number will be assigned following the provisions of the General Regulation on Management and Inspection Procedures. Please note that if the Spanish tax authorities do not issue a decision on the Spanish VAT number in a period of a maximum of three months since the application was made, it means that the request was denied due to various reasons.

Documents to be completed by Spanish VAT payers

Businessmen who want to open a company in Spain that is charged with the VAT should also be aware of the fact that if they have obtained their VAT number, additional requirements, other than the ones mentioned above, must be completed. In this sense, the company may need to complete the EC Sales List, a document that is also requested for the sale of services, not only for the sale of goods (starting with 2010); our team of consultants in company registration in Spain can provide more information on this document.

This document is generally requested if a Spanish company that was issued with a VAT number makes an intra-community supply. This document has to be completed on a monthly basis and it must be submitted to the local Spanish authorities. It is legally required to submit this document on a monthly basis as long as the value of the products is above EUR 35,000. In the case in which it is below this value, then the document can be submitted on a yearly basis.

It must be deposited on the 20th of the month, following the supply of goods or services. It is necessary to know that the document can be completed as a paper document, but in practice, the electronic document is more preferred. In the case in which the document is submitted later than the required deadline, there is a standard fee of around EUR 20, which is applicable for both late submissions and no submissions; investors can request more information on additional VAT-related documents from our team of specialists in company registration in Spain.

What are the VAT regulations for Spanish sole traders?

One of the ways to carry a commercial activity in Spain is by opening a sole trader. Since the sole trader does not represent a separate legal entity that its owner, the tax requirements and tax compliance measures are different than in the case of corporate entities. Sole traders in Spain that develop a taxable activity are thus, required to register for taxation, including for VAT.

The VAT registration in Spain in 2024 is compulsory for a sole trader if the services or the products sold by the company’s owner are liable for VAT. If so, the Spanish sole trader should prepare specific documents necessary for the payment of the VAT and submit them on a quarterly basis. If the sole trader is liable for various taxes, including for VAT, it must be registered with the Spanish Tax Office (Agentia Tributaria).

It is also worth knowing that the sole trader does not a Spanish VAT number, as the owner can use his or her NIE number (Numero de Identidad de Extranjero) for the same purpose, if the owner of the company is a foreign person. Our team of consultants in company registration in Spain can provide step-to-step advice to foreigners who want to register a sole trader in this country.

The video below offers more details on the IVA tax in Spain:

When should a company appoint a tax representative in Spain?

A foreign company selling products or services in Spain must also appoint a tax representative in specific situations. Those opening a company in Spain should be aware that the tax legislation in Spain require scompanies to have a tax representative in this country. The procedure is not applicable to entities that are tax residents in one of the EU member states, but it is compulsory in the case of entities outside the EU. However, the procedure is not necessary in the case of entities registered in one of the following: Melilla, the Canary Islands or Ceuta.

The procedures for appointing a tax representative in Spain have to be completed prior to engaging in any financial transactions in this country. The Spanish Tax Administration must be informed on the identity of the tax representative during the formalities for VAT registration in Spain and the basic condition to appoint a tax representative is that the respective person must have his or her domicile in this country.

As a tax representative of a foreign country operating in Spain, the person is legally required to complete all the company’s tax obligations that are prescribed under the national law. It is necessary to know that the tax representative does not have any obligations towards the Ministry of Finance in Spain and all the obligations that arise from this institution must be completed by the foreign entity.

Taxation in Spain

VAT returns in Spain must be filed periodically: the frequency is determined by the turnover. It can be monthly or quarterly. A VAT grouping regime allows companies to make aggregated VAT returns that includes the filings of more than one company in Spain.

Spanish companies also have other taxes to pay apart from the value added tax. The most important one is the corporate income tax. Our experts can give you more information regarding the General Tax Law in Spain and how your company must observe it. We can also help you with professional accounting services and assistance for filing and payment. Contact our specialists in company registration in Spain to find out more about how to invest in this country.