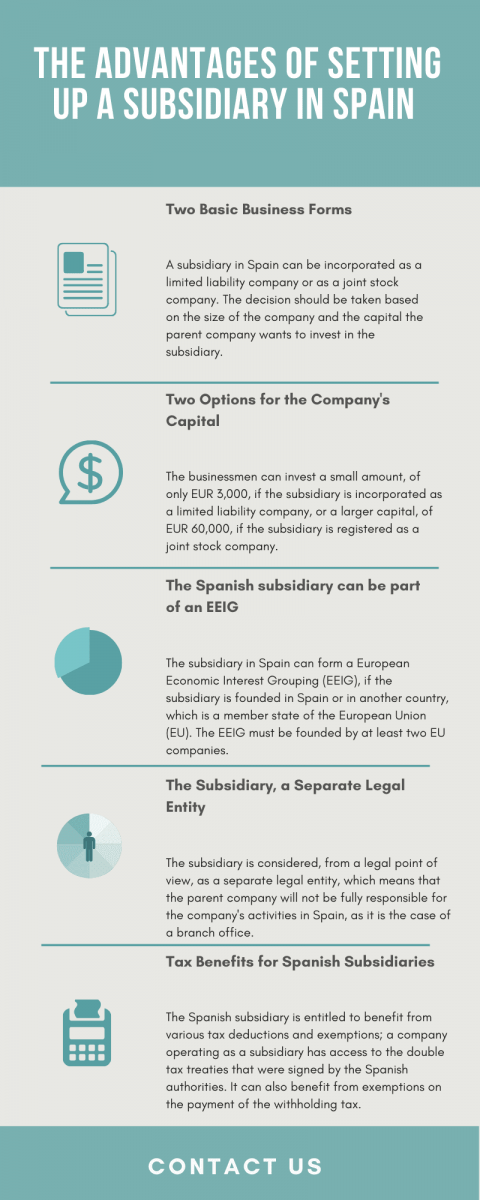

A Spanish subsidiary is a form of company in which the capital is owned by a foreign company. Even though the capital is provided by the foreign company, the subsidiary is considered a separate legal entity, and the liability of its shareholders is limited by their contribution to the capital. Our team of consultants in company registration in Spain can offer in-depth assistance on the procedure of opening a subsidiary in a Spanish city.

| Quick Facts | |

|---|---|

| Applicable legislation (home country/foreign country) |

Spanish Company Law |

|

Best used for |

– banking, – insurance, – automotive, – IT&C, – trading |

|

Minimum share capital |

Yes |

| Time frame for the incorporation (approx.) |

Around 2 months |

| Management (local/foreign) |

Local |

| Legal representative required |

No |

| Local bank account |

Yes |

| Independence from the parent company | Yes |

| Liability of the parent company | No, the subsidiary is fully liable |

| Corporate tax rate | 25% |

| Possibility of hiring local staff | Yes |

The taxation of a subsidiary may differ, depending on the existence of various international treaties. For example, no withholding tax on dividends paid to a foreign company from an EU country is imposed. Also, numerous double tax treaties signed by Spain stipulate that the profits are taxed only in the country of origin of the foreign companies.

Table of Contents

The rules for registering a Spanish subsidiary in 2024

A subsidiary established in Spain is seen legally as a local company and must follow the same rules stipulated by the Spanish Commercial Law. In order to open a subsidiary in Spain, the representatives of the parent company have to take a decision on the matter during the general meeting of the shareholders.

You can choose to open a subsidiary in Spain by forming an SL or Sociedad Limitada. The simplified tax regime is applicable under certain conditions.

The resolution must be legally translated into Spanish and must be accompanied by the certification from the specific Spanish consulate that the foreign company really exists and it’s legally constituted. The founders must check the subsidiary name at the Central Mercantile Register and reserve the available name, following the standard requirements imposed to other types of businesses that are registered in this country and our team of consultants in company registration in Spain can offer advice on this procedure. Below is an infographic with information about subsidiaries in Spain:

With regards to the registration of a company name, which is done through the Central Mercantile Register, one has to know that the institution will charge specific fees. In 2024, the application for a trading name certificate is around EUR 6, and the issuance of the certificate will cost EUR 6 as well. Parties interested in obtaining proof of the trade name certificate will be charged with EUR 1.5. Any other information that is of interest to a third party on a given company will be charged with various fees.

Is it necessary to open a bank account in Spain for the subsidiary?

A bank account must be opened and at least EUR 3,000 must be deposited by the investors if the subsidiary is registered as a limited liability company or 25% of the share capital if the business is set up in the form of a joint stock company (not below EUR 15,000). If the subsidiary will be set up as the latter mentioned business form, the share capital that has to be deposited is EUR 60,000.

The subsidiary’s founders must also draft the articles of association and notarize the document along with the other deeds (the decision of opening the subsidiary, the certificate of deposit). Investors who want to open a company in Spain have the possibility of granting the power of attorney to our specialists, who can conclude this procedure.

The next step in the process of registration of a subsidiary in Spain is receiving a provisional number of fiscal identification, after submitting the specific documentation to the National Tax Authority Delegation. A tax of 1% of the company’s capital, called transfer tax on stamp duty, must be paid at the general Directorate for Tax of the Autonomous Community. When opening a Spanish subsidiary, besides this tax, the company’s representatives also have to deposit the company’s statutory documents, together with a copy of the company’s fiscal identification number.

More details on the Spanish subsidiary are available in the video below:

Bookkeeping in Spain is an important part of accounting. Any company should consider such services offered by our certified accountants. A company’s financial operations must be recorded using specific procedures and documents, and an accountant can provide you with all the details. Our specialists can offer personalized services, depending on the company’s activities and needs.

What other procedures must be followed when opening a Spanish subsidiary?

During the procedure of company formation in Spain for a local subsidiary, it will also be necessary to register the entity with the Mercantile Register. In order to register with this institution, it is necessary to provide a set of documents and our team of specialists in company formation in Spain can help investors prepare the following:

- the decision of opening the subsidiary, alongside the consular certificate attesting to the validity of the foreign company;

- the documents of incorporation and, in this case, due to the fact that most of the subsidiaries are set up as limited liability companies, the required documents are the articles of association and the memorandum;

- the provisional number of fiscal identification, issued by the local authorities as mentioned above;

- a copy of the receipt of the payment made at the Directorate for Tax of the Autonomous Community.

Besides the above-mentioned steps, other procedures have to be completed when opening a company in Spain that will operate as a subsidiary. Investors can request full assistance on all the documents necessary in this case from our team of specialists in company registration in Spain, but it is necessary to know that businessmen will also have to provide a declaration of foreign investments (known as D1-A Form), a document that has to be deposited with the Registry of the Directorate General for Trade and Investment of the Ministry of Economy and Competitiveness.

A subsidiary in Spain based on an SL structure must have a minimum of 3 directors, but no more than 12, regardless of their nationality and residence.

What are the characteristics of the legal entities available for a Spanish subsidiary?

As we presented above, the Spanish subsidiary can usually take the form of two legal entities – the limited liability company (LLC) and the joint stock company (public limited company – PLC). The decision of incorporating a Spanish subsidiary depends on the capital the parent company wants to invest in the local business, but also on other factors, which are presented below. Our team of consultants in company formation in Spain can assist with advice on the most suitable business form available for a specific business scenario, but the following need to be considered:

- shares of the company – in the case of the LLC, the shares can’t be publicly traded, while in a PLC, the company’s representatives may trade the company’s shares;

- the transfer of shares – when forming a subsidiary as an LLC, the investors do not have the possibility of freely transferring the company’s shares, unless they are transferred among the members of the company and their close family relatives, while in the case of the PLC, the founders have the legal right of transferring the shares;

- appointing directors – in an LLC, the company’s directors can be appointed for an indefinite period of time, while in the case of PLC, they can be elected for a maximum period of 6 years;

- the structure of the board of directors – the subsidiary formed under an LLC must have a board of directors that is composed of a minimum of 3 members and a maximum of 12, while in the case of the PLC, the minimum requirement is the same as in the case of an LLC. Still, there is no maximum threshold applicable here.

Can a subsidiary in Spain form an EEIG?

Yes, a subsidiary in Spain or a subsidiary that is a tax resident of another country, a member of the European Union (EU), can form a European Economic Interest Grouping (EEIG). It is important to know that non-EU companies may also form an EEIG, as long as they operate through a subsidiary in the EU, which follows the EU legislation on the matter and which has central management at the level of the Community.

The main requirement for setting up an EEIG is that the companies forming this group have to be from different EU countries (at least two of the companies). Our team of consultants in company registration in Spain can provide more information on the advantages of starting an EEIG in this country.

The incorporation of a subsidiary in Spain in 2024, is made in about 2 months, respecting Spanish Company Law. One of our Spanish local agents can offer support in this endeavor.

What are the main Spanish taxes for companies in 2024?

Companies operating in Spain are liable to a set of corporate taxes, which is also applicable to a Spanish subsidiary. All Spanish companies are liable to the corporate income tax, which is imposed at the rate of 25%, as well as to the capital gains tax (applicable at the rate of 25%). Companies also have to pay the withholding tax, a tax that is imposed on dividends, royalties, and interest.

Companies are also imposed with the value-added tax (VAT), applied at the standard rate of 21%. However, depending on the services or products delivered by the company on the local market, lower VAT rates can be applied (available at rates of 0%, 4%, and 10%).

Other taxes, such as the real estate tax, the transfer tax, the stamp duty, and the social security contributions, can form the tax base of companies registered in Spain. Our team of agents specialized in Spanish company formation may further advise on any other taxes that can be applied to local businesses. It is necessary to know that the property tax and the stamp duty can have tax rates that vary depending on the Spanish region in which the transaction takes place, as well as on the value of the transaction itself.

Subsidiaries in Spain can benefit from a favorable taxation system and a stable fiscal climate, however, some changes must be implemented. You can discuss further details with one of our experienced agents about the tax structure applicable for foreign subsidiaries established in Spain.

Main advantages of starting a Spanish subsidiary

A foreign company wanting to expand in Spain can have a set of advantages when starting a Spanish subsidiary. For example, it will benefit from easier access to the Spanish market and other European markets. It can also be used as a manner of increasing the brand recognition of the mother company. Depending on the company’s specific activities, it can be used as a way of reducing certain operational costs, but it can also reduce its taxes through the double taxation treaties available here.

Owning a subsidiary in Spain requires a local administrative body. As such, the administrator must be a fiscal resident in this country. We mention that not having this kind of representative means that there are no activities carried out in Spain, as the Tax Agency might consider.

One should note that most expenses required for the economic operations of a subsidiary in Spain are deductible. This applies only if such expenses are not personal expenditures or employee expenses not linked to the company business in Spain.

Our company formation agents in Spain can offer you more details regarding the Mercantile Register and can help you establish a business in this country. Contact our representatives for further assistance.